For equipment-heavy businesses in Canada, traditional bank financing can feel like it was designed for someone else. You have hard assets, real revenue, and genuine growth opportunities — but your most recent financials don’t tell the whole story. That’s exactly the gap that asset-based lending is built to fill.

Asset-based lending (ABL) is a type of financing that allows businesses to secure a loan by using their physical assets as collateral — equipment, commercial vehicles, real estate, or inventory. Instead of relying primarily on credit history and cash flow statements, ABL lenders focus on the value of what you already own.

We sat down with Darren from Essex Lease Financial Corporation (ELFC), a Calgary-based direct lender with nearly 40 years of experience financing industrial equipment across Western Canada, to get an inside look at how ABL actually works — and why it’s become the financing option of choice for a growing number of Canadian businesses.

What Is Asset-Based Lending?

At its core, asset-based lending is the business of loaning money using business assets as collateral. As Darren explains it: “The assets we are lending against are at the heart of every solution we build for a customer.”

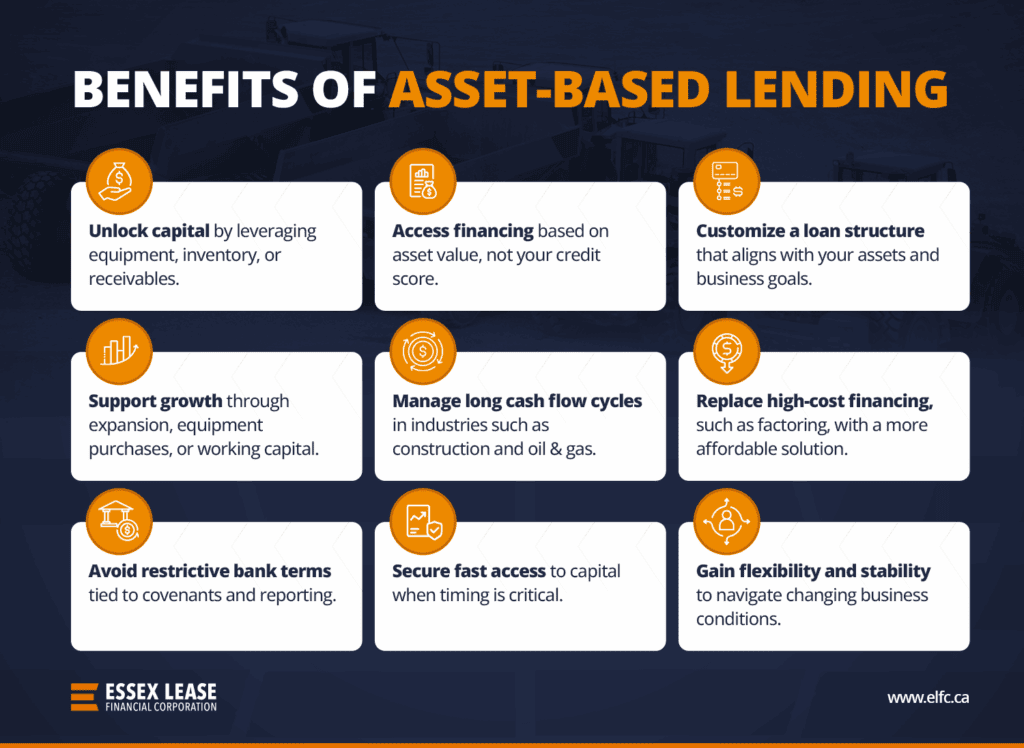

Unlike traditional bank loans, which hinge on financial covenants, receivables performance, and strict eligibility criteria, ABL takes a different starting point: the tangible value in your business. If you own equipment, commercial real estate, or other valuable physical assets, those assets can often be leveraged to unlock capital — regardless of whether your financials are perfectly polished.

This distinction matters enormously for businesses operating in capital-intensive industries. A trucking company that owns a fleet of semis, a construction firm with excavators and graders, or an agriculture operation with high-value machinery — all of these businesses carry significant asset equity that traditional lenders routinely undervalue or ignore.

How Does Asset-Based Lending Work?

The ABL process differs from a standard bank loan application in one fundamental way: the lender’s primary question is not “How strong are your financials?” but rather “What do you own, and what is it worth?”

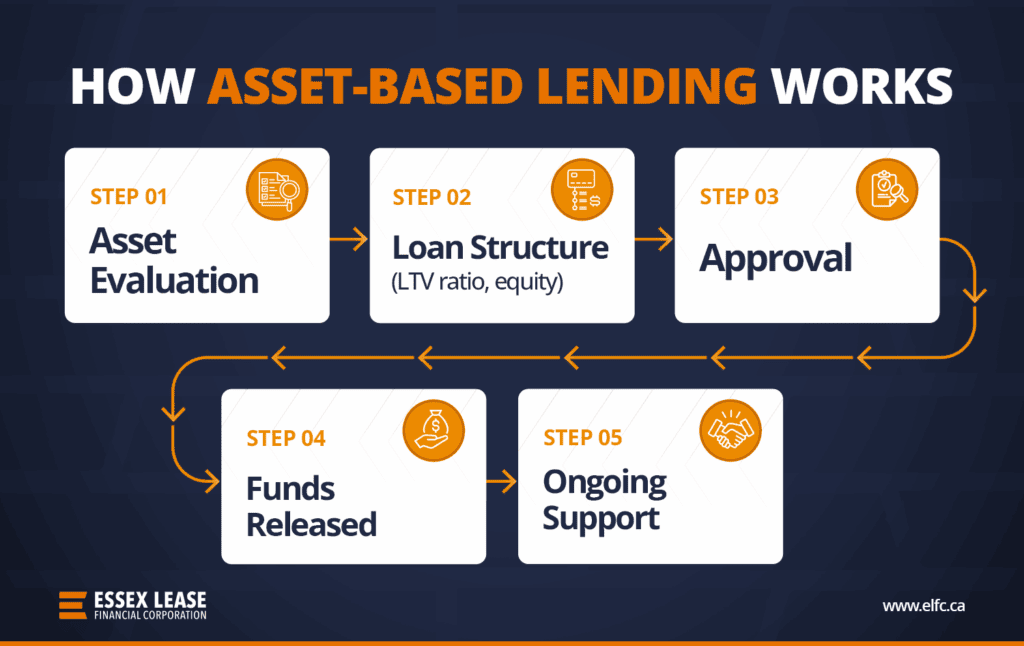

Step 1: Asset Inventory and Valuation

ELFC begins by understanding what assets your business owns — equipment, commercial real estate, or vehicles. The lender evaluates the current market value of those assets, factoring in age, condition, brand, and resale liquidity.

Step 2: Determine Your Borrowing Base

Your borrowing base is the amount ELFC is prepared to lend against your assets. Longer-life, slow-depreciating assets like heavy equipment and commercial real estate typically qualify for higher advance rates than short-lived or volatile assets.

Step 3: Structure the Right Financing Solution

Rather than fitting you into a standard product, ELFC builds a solution around your needs. As Darren notes: “We talk through the features, advantages, and benefits of all ELFC products to match customers with the right financing option.” This could mean:

- A term loan to unlock working capital from existing equity

- Refinancing existing equipment debt to reduce payments or free up cash

- Debt consolidation to simplify obligations and improve cash flow

- An Asset-Based Line of Credit (ABLoC) for ongoing, revolving access to funds

Step 4: Approval and Funding

Because underwriting is asset-focused rather than purely financial-statement-driven, decisions can move faster than with a traditional bank. ELFC can often turn around financing approvals within 48 hours.

Types of Asset-Based Lending at ELFC

ELFC’s ABL solutions span several structures, depending on what a business needs:

Asset-Based Line of Credit (ABLoC)

An asset-based line of credit is a revolving facility that allows businesses to draw against the equity in their assets as needed. Unlike a term loan, an ABLoC gives you ongoing access to capital — useful for managing seasonal cash flow swings or funding growth without selling assets.

Equipment Refinancing

If you own equipment that is paid off or has significant equity, refinancing unlocks that equity as usable capital. This is a common tool for businesses looking to fund expansion without taking on new debt obligations or diluting ownership.

Debt Consolidation

Businesses carrying multiple loans or lease obligations can consolidate into a single, structured ABL facility. This simplifies payment management and often improves cash flow by extending amortization or reducing the overall interest burden.

Working Capital Lending

For businesses that are asset-rich but cash-constrained — a common situation in construction, oil and gas, and agriculture — ABL can provide the working capital needed to cover payroll, materials, and operating costs without waiting for receivables to convert.

Who Benefits Most from Asset-Based Lending?

ABL is not just for businesses in financial distress. As Darren is clear to point out: “Any business with hidden or locked equity in their equipment that wants to use it to drive growth or expansion can benefit.”

You may be a strong candidate for ABL if your business:

- Owns equipment, commercial vehicles, or real estate with clear value

- Operates in a capital-intensive industry where assets accumulate faster than cash

- Has strong operational fundamentals but a short credit history or imperfect financials

- Needs faster access to capital than traditional banks can provide

- Is in a growth phase and needs to invest ahead of incoming revenue

- Carries existing debt that could benefit from consolidation or restructuring

Industries that commonly use ABL at ELFC include:

- Transportation and trucking

- Construction and aggregates

- Oil and gas services

- Agriculture and farming operations

- Forestry and logging

- Manufacturing and industrial operations

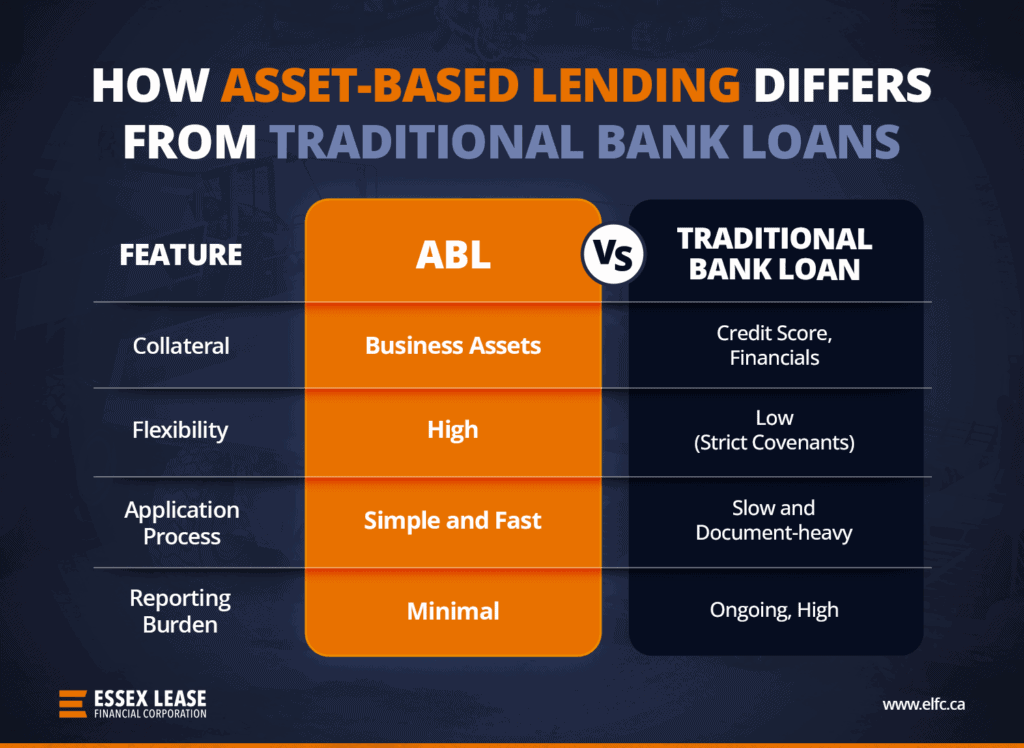

Asset-Based Lending vs. Traditional Bank Financing

Understanding the difference between ABL and a conventional bank loan helps clarify when each option is appropriate:

| Asset-Based Lending (ELFC) | Traditional Bank Loan | |

|---|---|---|

| Primary underwriting basis | Value of assets / collateral | Cash flow + credit history |

| Speed of approval | Often 48 hours | Weeks to months |

| Flexibility of structure | High — customized per client | Low — rigid templates |

| Financial covenant requirements | Minimal or none | Extensive |

| Works for challenged credit? | Often yes | Rarely |

As Darren explains, the cost comparison isn’t always straightforward: “A properly structured asset based loan is always better than a low-rate option with restrictive loan terms.” When you factor in the opportunity cost of missing a growth window because your bank said no, the total cost of traditional financing is often much higher than it appears.

Common Misconceptions About ABL — Debunked

“ABL is only for struggling businesses.”

Not true. ABL is a strategic financing tool used by growth-oriented companies as readily as it is by businesses navigating a cash flow challenge. If you have equity locked in your assets, ABL is simply an efficient way to put that equity to work.

“Asset-based loans are always more expensive.”

This overlooks the real cost of traditional bank covenants — including the compliance burden, reporting requirements, and the restrictions they place on business decisions. A well-structured ABL facility can deliver better total value even at a nominally higher rate.

“You need perfect credit.”

ELFC, as an independent lender, looks at the broader picture. Character, business model, asset quality, and long-term potential all factor into lending decisions. A business with a strong operating track record can often qualify even if its most recent financials don’t reflect peak performance.

“The process takes too long.”

ELFC is not a large bank bureaucracy. Approvals can often be completed in 48 hours — far faster than the weeks or months that conventional bank processes typically require.

Why More Canadian Businesses Are Turning to ABL

Access to flexible business financing has never been more critical — and traditional banks are increasingly falling short for established businesses. According to a 2024–2025 government review, 75.8% of government-backed small business loans in Canada would have been denied by conventional lenders without program guarantees.1 Banks have also tightened credit standards for 13 consecutive quarters.2

The alternative lending market in Canada — of which ABL is a core component — is responding to this demand. The sector reached USD $2.17 billion in 2024 and is projected to grow at a CAGR of 17.9%, reaching USD $4.2 billion by 2028.3 Globally, the ABL market is expected to grow from $785 billion in 2024 to over $1.4 trillion by 2029.4

For Canadian industrial businesses, this shift represents both a challenge and an opportunity. Banks are getting more selective. Independent lenders like ELFC are stepping in to fill that gap — not as a last resort, but as a first-choice financing partner for businesses that need flexibility and speed.

How to Get Started with Asset-Based Lending

ELFC simplifies the process. To get started, it helps to have:

- A list of owned assets (equipment, vehicles, real estate) with approximate values

- A clear understanding of what you need financing for — working capital, growth, or consolidation

- Basic business and operational information

- Openness to exploring different financing structures

As Darren puts it: “Find a lending partner who spends more time asking questions about your company and your needs than they do talking about themselves.” You don’t need to show up with perfect financials — you need to show up with a clear picture of your assets and your goals.

Want to explore your asset-based lending options? Contact Essex Lease Financial Corporation today to discuss your financing needs.

Final Thoughts

Asset-based lending is not a workaround — it’s a fundamentally different philosophy of business financing. It starts with what your business has built and asks how that equity can be deployed to help it grow further.

For businesses in transportation, construction, oil and gas, agriculture, and other industrial sectors across Western Canada, ELFC has spent nearly 40 years developing the expertise and flexibility to structure financing that actually fits. The assets you’ve invested in shouldn’t sit idle on your balance sheet when they could be working for your business.

Sources

1 Greenbox Capital — Rise of Alternative Lending: Canada vs. U.S. (2025).

2 Greenbox Capital — Federal Reserve Small Business Credit Survey data, 13 consecutive quarters of credit tightening by banks.

3 Research and Markets — Canada Alternative Lending Market Report (2024).

4 The Business Research Company — Asset-Based Lending Global Market Report (2025).